NEW BOOK PROVIDES ROAD MAP FOR AMERICA TO AVOID ECONOMIC COLLAPSE

Greece, Argentina, and the old Soviet Union had governments that were Ponzi schemes that eventually went bust. A Ponzi scheme, named after the swindler Charles Ponzi (1882-1949), is an investment fraud that pays existing investors with funds collected from new investors — often with the promise of high returns.

In a new book, “The Greatest Ponzi Scheme: How the U.S. Can Avoid Economic Collapse,” Leslie A. Rubin and Daniel J. Mitchell provide a well-written and informative history of how much of the world and particularly the United States managed to get into the current fiscal mess. The pessimistic part of the book is the discussion of what will happen if we stay the present course. The optimistic side of the book is a description of a number of success stories, along with a policy path that almost any country can follow to revive.

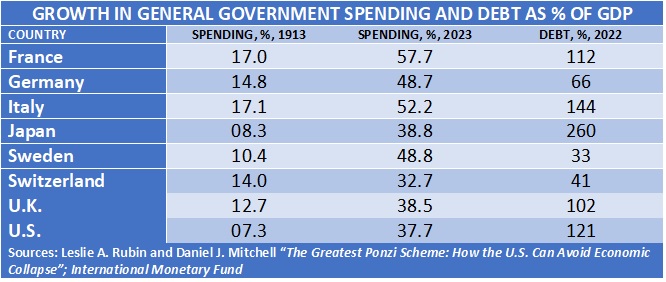

The villains are the political class in almost every country who enjoy spending other people’s money for their direct enrichment or to buy votes and power. British Prime Minister Margaret Thatcher said it best: “The problem with socialism is that you eventually run out of other people’s money.” Before World War I, government spending in almost every country was a small share of gross domestic product. Centralized countries like France and Italy did most of their government spending at the national level, while decentralized countries like the U.S. did most of their spending at the local or state level. Either way, government spending was a much smaller share of people’s lives.

In the United States, things began to change in the 1930s with the development of welfare programs, notably Social Security. At the time, the Social Security tax rate was very low, along with a few years of work requirement to qualify for benefits at age 65. Like any good Ponzi scheme, it promised a huge lifetime payout for a relatively small tax payment. (Social Security taxes were first collected in 1937, and monthly benefit payments began in 1940.) In 1937, the average American man lived to be 58, and the average American woman lived to be 62. As of 2023, it was 74 for men and 80 for women.

So, back in 1937, Social Security was a very low-cost program — in that the average life span was less than 65. If you were lucky enough to live well into your 80s, like my own grandparents, you hit the lottery — many years of benefits for a relatively small total tax payment over two or three decades.

We are now on the flip side of the Social Security scam because our children and grandchildren will be paying high Social Security taxes for a program, if it even survives, providing benefits in increasingly depreciated dollars.

In addition to Social Security, Mr. Rubin and Mr. Mitchell review many of the so-called entitlement programs that are the real budget busters. The payments from these programs consistently grow faster than the economy or tax revenue and now consume the bulk of the federal budget. Anyone who can do basic math can quickly understand the problem. When a country reaches the point where it is borrowing just to pay interest on the debt, game over. The remaining question is how much longer before there are no new bond buyers.

The Greeks were living well on borrowed money until 2009 — but then the lenders stopped lending, realizing they were unlikely to get their money back. Having no choice, the Greeks cut back on government spending, and much of the hoped-for private investment stopped. The result was a deep decline in consumer incomes, and now years later the shortfall has still not been made up. Greece, being part of the eurozone, was unable to print money (as Argentina did) to temporally appear to cover its shortfalls. Argentina followed the classic way of covering its deficits — by just printing money — which, predictability, led to higher and higher rates of inflation. Both Argentina and Greece are still struggling to downsize their governments to levels that bond buyers feel are sustainable.

Fortunately, there are a number of success stories that serve as role models of what to do. When the Soviet Union collapsed in 1991, most of its citizens lost their life savings and were impoverished, including those in the captive nations of Estonia, Latvia and Lithuania. These Baltic countries went through radical economic reform, including establishing relatively small governments. Estonia now has the lowest debt-to-GDP ratio in the world among non-petro-state developed countries and enjoys a high, Scandinavian-like standard of living.

Switzerland is perhaps the best model for fiscal responsibility in a highly developed country, in that for the most part the Swiss keep government spending growing no more rapidly than the private sector. Despite being landlocked with few natural resources, Switzerland enjoys a higher per capita income than the U.S. and both a stable fiscal and monetary situation.

Mr. Rubin and Mr. Mitchell have done a great service in providing a highly understandable book, outlining the disaster about to engulf us if we do not change quickly, but equally important, a road map for getting out. Every policymaker and concerned citizen ought to buy this book and refer to it often — an economic bible of sin and salvation.

• Richard W. Rahn is chairman of the Institute for Global Economic Growth and MCon LLC.

https://www.washingtontimes.com/news/2024/mar/18/are-you-part-of-ponzi-scheme/

© Copyright 2024 The Washington Times, LLC.