INFLATION IS HERE TO STAY, BUT INNOVATORS WILL HELP MITIGATE SOME OF ITS PAIN AND DESTRUCTION

Where does the world economy go? Inflation is rampant, with a global recession almost a certainty. And then there is the problem of endless growth in government — that saps our personal liberties and economic vitality. It is a trend that cannot continue, so it will stop.

The problem is particularly acute in democracies, where the people have learned they can vote themselves “free stuff.” Increased reliance on a government welfare state and the employer of last resort is addictive, and politicians who preach and try to practice fiscal restraint are often voted out.

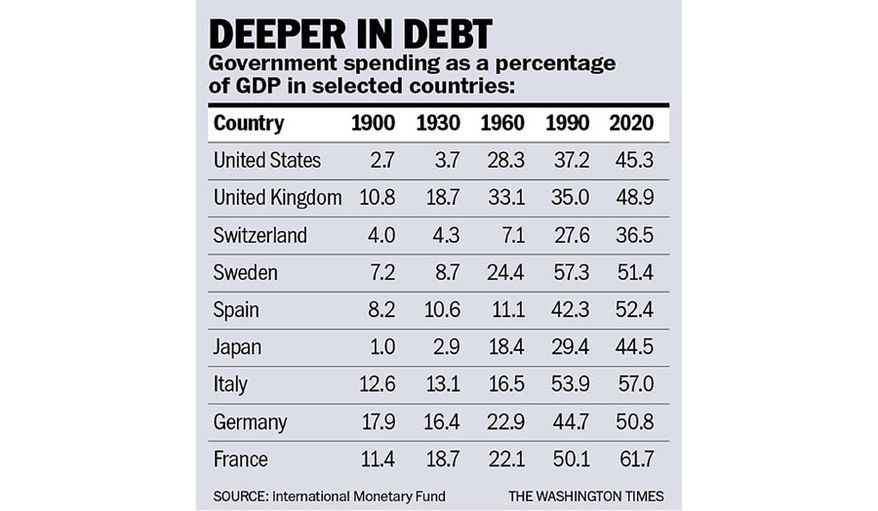

The accompanying table shows the growth in government spending in major developed democracies. France, Italy, Japan, the U.K. and the U.S. have government debt burdens that now exceed 100% of their GDP, and only Sweden and Switzerland have been able to keep their debt burdens under a very manageable 50%. (Note: the numbers come from the IMF, and measures of GDP and definitions of government spending are often inconsistent between countries. The 2020 numbers are slightly overstated due to the pandemic shutdowns — but the trend toward bigger government almost everywhere is what is important.)

In 1900, the U.S. had a very small federal government. Other than supporting a modest army and navy, it did almost nothing. No big welfare or retirement programs. Two-thirds of government spending was done by state and local governments. There was a big surge in spending during World War I, but immediately afterward, the government and particularly the military was sharply downsized.

In the mid-1930s, under the influence of the economist John Maynard Keynes, governments increased spending, to be financed by an increase in debt, for the explicit purpose of reducing unemployment. Keynes and his followers argued that the “employment programs” were intended to be temporary, and as soon as full employment was reached, the additional tax revenue would be used to pay off the debt that was incurred. The political class around the world loved the Keynesian model because it gave them the endless excuse to spend more money and accumulate more power — all in the name of doing good and increasing prosperity.

Socialism had been on the rise, particularly in Europe, and many industries were nationalized. Keynes was not a socialist, but by justifying what became the welfare state, socialism became more respectable, particularly in his native Britain. By the late 1970s, it became obvious that the socialist and Keynesian prescriptions were not working as advertised, but the addiction to government spending was too widespread and attempts to roll it back by leaders like Margaret Thatcher and Ronald Reagan met with only limited success.

Big Government not only reduced civil and economic liberties but, by putting enormous additional overhead costs on the private sector, slowed economic growth. The governmental economic drag became apparent by the 1980s, and the empirical evidence increasingly showed that as the government grew as a share of GDP, the dead weight loss from the government kept growing until growth stopped. This, not surprisingly, is particularly true of countries with very high debt burdens — notably Japan, France, Italy and the U.S. — that are being financed by inflation, limited spending reductions and/or higher taxes — all of which are impediments to growth. Growth appears to have already stalled out in these countries, with others likely to follow in the next few months. Growth almost everywhere should have been very rapid coming out of the pandemic shut down. Yet, the initial surge of growth has been insufficient to even make up for the job losses suffered during the pandemic.

Many of the same people who argued that the inflation was “transitory” are the same people who are now arguing that any recession will be minor and short-lived. For that to happen, much of the debt is going to have to be worked off quickly, and the tax and regulatory impediments that are strangling both the U.S. and world economy will need to be removed. Do you see any major political leader who is specifically proposing what needs to be done?

Inflation can greatly increase the effective capital gains tax rate, even though there has been no legislative vote to increase the tax. (States like California and New York, which rely heavily on capital gains taxes on “the rich” for a disproportionate share of their revenue, are in for a rude awakening next year as “the rich” start reporting massive capital losses rather than gains.)

The good news is that there are people like Elon Musk who have the imagination and ability to see and create new things to make life better. Artificial intelligence, the blockchain, private asset-backed digital currencies and other things that will be invented will mitigate some of the destruction and pain caused by the political class. A slim reed of hope, but better than no reed at all.

• Richard W. Rahn is chairman of the Institute for Global Economic Growth and MCon LLC.

https://www.washingtontimes.com/news/2022/jun/27/pressures-of-big-government-spending-offer-little-/

© Copyright 2022 The Washington Times, LLC.